The global smartphone market continued its growth trajectory in Q1 2025, with a 3% year-over-year increase in sell-through volumes, according to the latest findings from Counterpoint Research’s Market Pulse Early Look. This growth was primarily driven by emerging markets and subsidy-led demand in China, despite showing signs of potential decline for the remainder of the year.

Apple Takes Historic Q1 Lead as Samsung holds its own

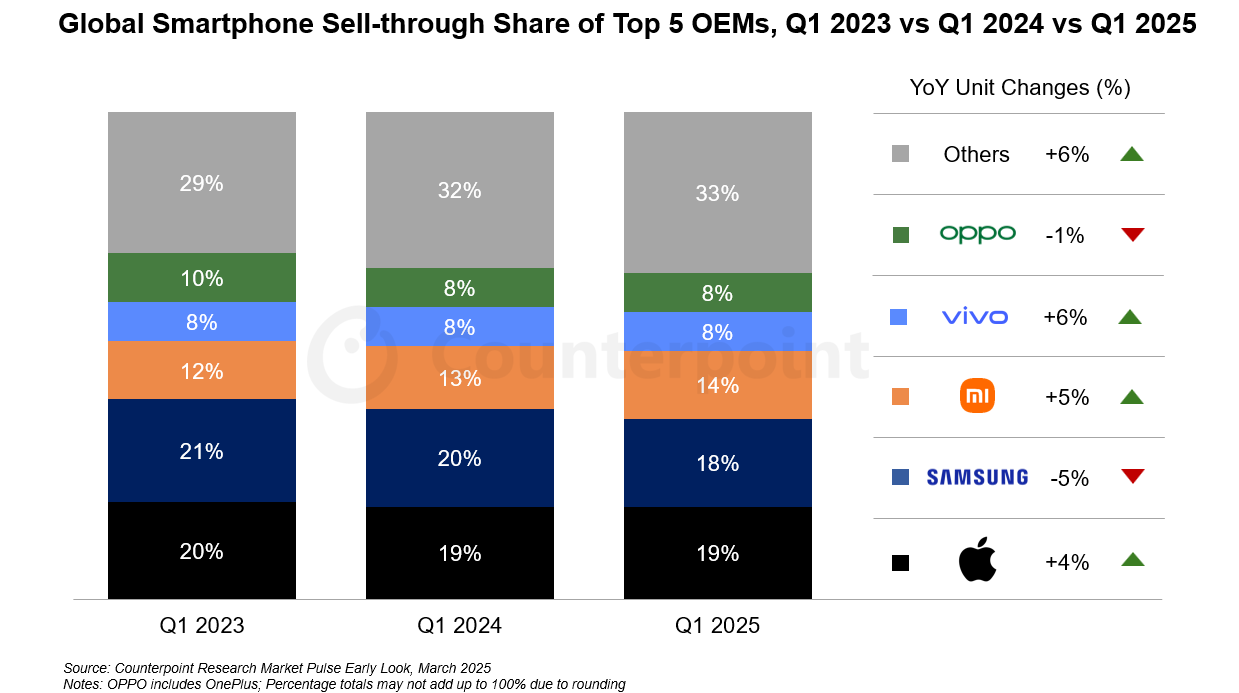

For the first time in a first quarter, Apple secured the top position with a 19% market share, outpacing traditional Q1 leader Samsung. This milestone achievement comes on the heels of Apple’s iPhone 16e launch—an unusual release timing for the company—and its strategic expansion in emerging markets. While facing challenges in its core markets of the US, Europe, and China, Apple recorded impressive double-digit growth in Japan, India, Middle East and Africa, and Southeast Asia.

Samsung followed closely behind with an 18% market share. After a slow start due to the delayed launch of its flagship S25 series, the Korean giant saw a significant resurgence in March with double-digit growth. The company also reported an increase in the share of premium “Ultra” models within its S25 series sales, indicating strength in the high-end segment.

No Shaking for Chinese Manufacturers

Xiaomi continued its strong sales momentum, gaining market share through both domestic growth and international expansion. The brand’s successful entry into the electric vehicle market has enhanced its premium brand positioning in China.

Vivo climbed to fourth place, benefiting from high exposure to the growing Chinese market and strategic moves into emerging markets. OPPO rounded out the top five, with notable sales growth in India, Latin America, and Europe.

Outside the top five, HONOR, Huawei, and Motorola are providing increasingly tough competition globally. Huawei claimed the top spot in China for Q1, while HONOR and Motorola demonstrated significant growth across multiple markets.

Cautious Forecast for 2025

Despite the positive start to 2025, Counterpoint Research has revised its full-year forecast, now expecting a slight year-over-year decline in global smartphone volumes for 2025. This adjustment comes in response to rising economic uncertainties, particularly those caused by tariffs that are likely to impact consumer demand across markets, with the US expected to be especially affected.

“The market got off to a mixed start in 2025,” explains Senior Research Analyst Ankit Malhotra. “Q1 saw continued improvement in economic conditions, particularly in emerging markets. But mature markets like North America, Europe, and China showed signs of fatigue after a recovery in 2024.”

Malhotra noted that while January sales were particularly strong due to subsidy-led demand in China, and major launches like Samsung’s S25 and iPhone 16e maintained momentum, the situation quickly changed as economic uncertainties and trade war risks mounted toward the end of the quarter.

The global smartphone market has shown steady growth following a decline in 2023, primarily driven by improving macroeconomic conditions. While smartphones remain essential products with relatively stable sales, economic uncertainties can lead consumers to postpone purchases. Rising trade risks and supply chain disruptions could negatively impact the market in the coming months.

Despite these challenges, the proliferation of new technologies such as GenAI and foldable devices is expected to continue, though manufacturers will need to carefully monitor demand. Counterpoint Research maintains a steady long-term outlook for the industry, despite the projected decline in 2025.

As competition intensifies and market dynamics evolve, smartphone manufacturers will need to adapt their strategies to navigate the complex landscape of consumer preferences, economic factors, and technological advancements in the remainder of 2025 and beyond.

Paul Balo is the founder of TechBooky and a highly skilled wireless communications professional with a strong background in cloud computing, offering extensive experience in designing, implementing, and managing wireless communication systems.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok

{kind=link}